At first, the market was happy to reward big capex forecasts (META); but just a few days later, it changed its mind and decided that the bigger the beat, the bigger the penalty (as was the case with GOOGL today). That leaves Amazon in a precarious place as it prepares to report earnings after the close today: does it project some berserk number or does it risk being conservative? After all, the only thing that will matter is the capex forecast (the earnings will likely be good enough).

Looking at the bigger picture, Bloomberg notes that it’s probably not a great sign that Amazon’s share price is down more than 4% on the day of earnings, before the first headline has even hit. After the hyperscalers Microsoft and Alphabet spooked markets with their huge spending plans -- Meta seems to have got away with it -- perhaps the best thing Amazon could do would be to announce that it plans only moderate capital expenditure in 2026.

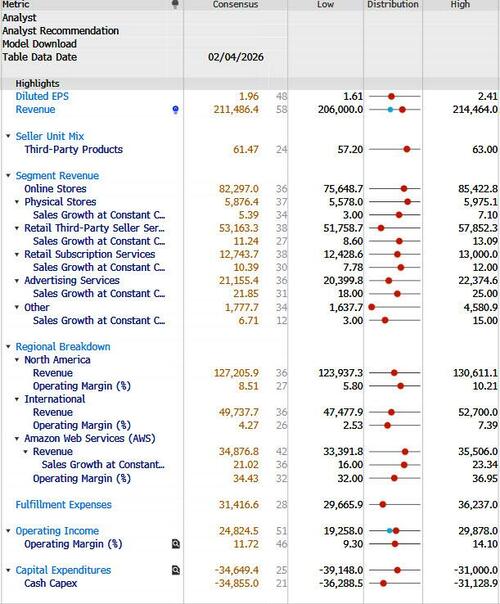

One thing in Amazon’s favor is that analysts aren’t really projecting too much growth. The consensus is that diluted earnings per share rose just a bit over 5% year-on-year to $1.96 in the fourth quarter. That’s little-changed from $1.95 in the third quarter. Revenue at Amazon Web Services is expected to have increased 21% to $34.9 billion, but that’s still less than half the revenue the company gets from its main business: online stores. Growth there is expected to be slower at roughly 9% year-on-year.

Its business mix explains why Amazon is so much less profitable than its peers and why the profitability of the cloud business will be key.

Capex aside, here is a preview of what JPMorgan's trading desk expects:

AMZN PREVIEW – AWS Acceleration & AI Positioning

SENTIMENT – Bullish, But Concerns Remain. Conversations & focus heavily AWS-skewed, no change there. 3Q EPS & re:Invent provided clarity on capacity expansion, supply from NVDA, Trn 2/3 performance & rollout, Rainier timing & doubling. Investor focus on degree of acceleration & cloud industry $ re-capture. AWS price increases suggest strong demand. But concern remains around AMZN’s overall AI positioning/strategy, relative gap to Azure/Google Cloud growth, & Trn adoption. Strong Stores execution expected, along w/NA & Int’l margin expansion.

The stock remains a Best Idea for JPM stgrategist Doug Anmuth." We remain bullish on AWS growth acceleration driven by core cloud growth & ramping AI contribution led by Project Rainier, Trn ramp, & new partnerships. N.America & Int’l OI margin expansion, solid AWS margins (though likely down Q/Q), & cost discipline support healthy FCF growth in ’26 even against AI-driven capex growth. Valuation attractive on GAAP P/E & FCF.

FOCAL POINTS –

- Accelerating growth on: 1) Project Rainier/Anthropic ramp; 2) increased capacity doubling by 2027; 3) Tr2 performance & Tr3 ramp; 4) core workloads/tech migrations

- More backlog growth in October than all of 3Q…OpenAI partnership could expand

- Watching $ growth Q/Q & Y/Y

- AWS pushbacks: 1) mid-20’s%+ AWS growth could come w/Azure & Google Cloud growing 2x that rate; 2) Tr chip rollout still early & needs bigger adoption beyond Anthropic; 3) Anthropic cloud/compute diversification

- Stores executing well w/8% holiday e-comm growth from Visa & Adobe slightly above

- Lower cost to serve on robotics/automation & inbound improvements

Takeaway from the recent JPM survey – AMZN: Favorite Mega Cap (46% of respondents)

According to UBS strategist Dwyer, the most prominent question since 3Q she has gotten is, “Why isn’t this up more?” Her response is "that was market-related exiting the year or maybe investors were waiting for one more quarter of strong execution before backing, but for a long list of reasons it’s pretty clear that it is structural reacceleration and not just a one-time event."

Here are UBS's buy-side Bogeys which the company will have to overcome:

- Q4 AWS Growth: up 22-23% y/y

- Q4 EBIT: $26.5-27 bn versus guide $21-26 bn/ around 11% margin at midpoint

- Q4 Total Sales: high end of guide $206-213 bn/ around 10-13% y/y

- Q1 EBIT Guide H-E: $22.5-23 bn

- Q1 Total Sales Guide H-E: $176-178 bn

And the sellside consensus

Loading recommendations...