Authored by Lance Roberts via RealInvestmentAdvice.com,

Rally Begins As Doves Emerge

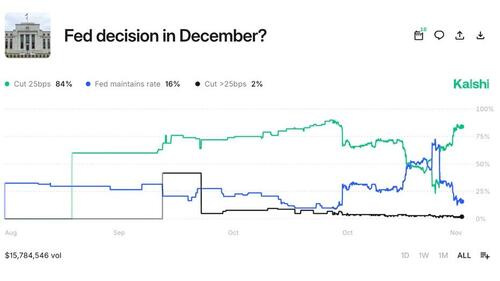

Markets surged into the Thanksgiving holiday, ending the week with substantial gains across all major U.S. indexes. The S&P 500 rose by approximately 3.7%, marking one of its strongest weeks in the past six months. The catalyst was a combination of falling bond yields and increasing confidence that the Federal Reserve has completed its rate hikes. Currently, Kalshi (prediction market) is projecting an 80% chance of a rate cut in December.

With inflation data continuing to trend lower and growth indicators remaining stable, the markets are starting to price in stronger earnings and economic growth in 2026, particularly as lower Treasury yields boosted duration-sensitive sectors and encouraged risk-on behavior.

Unsurprisingly, despite all of the recent talk of the “Death of the AI Trade,” Technology stocks once again led the charge. The AI narrative regained momentum, pulling mega-cap names higher and lifting the broader Nasdaq. Nvidia’s earnings beat helped reinforce the bull case around AI infrastructure and cloud demand. The “Magnificent Seven” tech leaders contributed outsized returns to index performance, though broader participation remained limited.

Volatility declined as technical indicators turned more supportive after the last few weeks of choppy action, which was also unsurprising. Despite the gains, many risks remain, including concentration in the market-cap-weighted index, valuations, and market breadth. However, those concerns may take a backseat temporarily following the recent correction and reversal in bullish sentiment.

Heading into December, all eyes will turn to the upcoming PCE inflation report, jobs data, and the final round of Fed comments before the blackout period. Until then, momentum favors the bulls, but the foundation remains fragile.

Year-End Rally Begins

In last week’s #BullBearReport, we discussed how the market becomes more predictable as we approach year-end. To wit:

“Heading into December, the seasonal tailwinds remain intact, as noted above. December is historically the best month for equities, with the “Santa Claus rally” often delivering average gains of 1.5% to 2.0%. With corporate buybacks in full swing, adding $5-6 billion in daily volume, investor positioning remaining stable, and professional managers underweight in exposure, particularly in technology companies, the fuel for a rally is present. However, the market also remains fragile due to poor underlying breadth and rising volatility, so caution is advised.

The near-term outlook is constructive, provided the Fed remains quiet and bond volatility remains contained. But any surprise, in inflation, growth, or geopolitics, could shift sentiment quickly. The key for investors is discipline. Don’t chase the rally blindly. Stick to quality, stay diversified, and use elevated prices to trim into strength where appropriate. While the potential for a year-end rally is higher after the recent correction, nothing is guaranteed.”

As discussed in the “Market Brief” above, the rally appears to have begun. November and December have historically shown a strong performance bias since 1950, with the S&P 500 posting gains in roughly 75% of the years. This period accounts for a disproportionately large share of annual returns.

The drivers aren’t mysterious. Mutual funds and institutions close their books on the calendar, or fiscal year, so there tends to be a push to catch up on exposures to certain stocks or sectors before year-end reporting goes out. This is commonly referred to as “window dressing,” but it does add support for the markets in the near term. Furthermore, as noted, investment managers who have underperformed try to play “catch-up,” so they rotate into the winners. “Beating the Market,” which isn’t a financial goal, has been incredibly difficult this year, as only 37% of the index is actually outperforming. As a result, mega-cap stocks and growth names are likely to be chased into the end of the year. That’s performance chasing, not investment strategy, but it still moves markets.

Lastly, retail flows also increase as post-October corrections tend to shake out weak hands. When that fear subsides, sidelined cash looks for a home, and retail investors tend to add to the buying pressure in November. We commented on this behavior in our October newsletter, “Year-End Rally, 3-Reasons To Buy The Dips,” we said:

“Furthermore, the “retail demand” remains consistent in 2025, and every dip continues to be bought aggressively. We can visualize this retail investing “BTFD” momentum trade. The following chart shows the “buying panic” that has occurred since the “Pandemic Shutdown” for investors under the age of 40, which dwarfs all other periods in the data set. While the eventual reversion is likely massive, by year-end, there is likely very little that can break the current psychology driving markets.”

As we stated in that mid-October newsletter, investors should have expected the recent pullback.

“Strong earnings, aggressive buybacks, and trend-following behavior provide a durable backdrop for the stock market rally to continue. Pullbacks should be expected, but they are more likely to serve as buying opportunities than signals of a larger trend reversal.“

That’s precisely what’s happened, and Thanksgiving week is usually the kickoff. Over the past decade, the S&P 500 has been green during Thanksgiving week in seven out of ten years. This year, that rally appears to have started early with Technology, small caps, and crypto turning higher.

As noted in the Technical Update above, the much-needed corrective action in the first half of November relieved the overbought conditions impacting the market, providing a better base for a year-end rally.

Tailwinds and Why the Correction Set Up This Move

With the majority of selling pressure having exhausted itself over the last few weeks, the backdrop for a year-end rally has improved. The setup is no longer dominated by panic-driven selling or forced de-risking, but, instead, several identifiable tailwinds are providing the necessary fuel for sustained upside. These forces don’t guarantee a rally, but they reintroduce one critical factor that had been missing: consistent buying power.

One of the most critical catalysts is the return of corporate buybacks, which, since 2000, has accounted for nearly 100% of net equity purchases. As shown, there is a very high correlation between corporate share buybacks and stock market returns. Now, with earnings season mostly complete, blackout periods have ended, and companies, particularly the mega-caps, are now stepping back in as steady buyers of their own stock. According to Goldman Sachs, daily buyback demand is expected to exceed $5 billion through early December. That kind of structural bid creates a firm floor under prices, especially in a low-volume environment.

Another overlooked factor is the cessation of CTA-driven selling. These computer-driven trend followers were net sellers throughout the recent correction. As they unwind bearish positions and shift to neutral or net-long exposure, the pressure flips. What was previously a source of downside has now become a source of upward momentum. Furthermore, hedge funds have been aggressive net buyers of equities in recent days to gain exposure to the market.

Earnings also play a key role in a year-end rally. With earnings season behind us, where expectations heading into Q3 were low, most of the bearish concerns have been laid to rest. Over 75% of companies beat estimates, 74% beat revenues, and 61% beat on both, which was well above the historical averages. More importantly, profit margins didn’t collapse, and forward guidance, while cautious, remained optimistic. That helped reset sentiment and reduce fears of an imminent earnings recession.

Finally, retail investors showed up to “buy the dip,” as they have done continuously this year. Such is also not surprising over a holiday-shortened Thanksgiving trading week when trading volume is lighter because institutional traders are away, leaving the “inmates to run the asylum.”

While there are undoubtedly many concerns heading into 2026 that investors should be aware of, over the next few weeks, several catalysts suggest that the “pain trade” is likely to be higher.

Is that a guarantee? Absolutely not.

Does that mean the markets can pull back in the first couple of weeks of December when mutual funds distribute their gains and incomes for the year? No.

However, the data does suggest that the market will likely have a positive bias into year-end, and dips should be used opportunistically.

Key Catalysts Next Week

Next week marks a pivotal moment for investors. The bulk of U.S. economic data is expected to resume after recent delays. Liquidity remains seasonally light. That raises the stakes. A few data points and events could drive outsized volatility. They also carry the potential to reinforce or derail the market’s year‑end setup. Below is a table of the most important market and economic events to watch.

The first week of December reconnects markets with key economic data that had been delayed during the recent government shutdown. The arrival of those data releases reactivates the fundamental underpinnings of market direction. A few strong prints — on inflation, employment, manufacturing, or services — could validate a bullish year-end narrative. Conversely, any surprise weakness could derail current optimism. Inflation data is especially sensitive, and the upcoming PCE release is expected to shape market expectations ahead of the next Fed meeting on December 9–10.

Liquidity remains thin with many traders still on holiday or in partial holiday mode. In such an environment, headline‑driven moves can be magnified. That means surprises, either good or bad, have the potential to move markets significantly more than usual. Lastly, with this being the last week before the Fed’s policy blackout period, any public statements from officials carry extra weight. Market participants will scrutinize every word looking for any tone or messaging that will influence yield expectations, risk sentiment, and positioning as we head into the final stretch of the year.

Bull Vs Bear

Over the last few weeks, we discussed the risk of downside pressure in the market and that the correction set up potential for a rally during the holiday-shortened trading week. That occurred with the S&P 500 rising roughly 3.7% from last Friday’s close near 6,849. That rebound recaptured the losses from the prior AI- and rate-cut-wobble selloff and pushed the index back toward its late-October highs. On a bigger picture basis, the index remains up around 16% year-to-date and is now roughly flat for November, reflecting a strong tape that has simply been digesting earlier gains. The rally also triggered a fresh momentum “buy signal” which will be supportive of further gains into next week.

From a trend standpoint, the price remains aligned with the bulls. The S&P is trading above its rising 50- and 100-day moving averages, which sit roughly in the 6,700–6,575 zone, and well north of the 200-day moving average near 6,175. Earlier in November, the index finally broke its streak above the 50-day moving average (DMA) and corrected back to the 100-DMA, working off some of the speculative excess in AI and high-beta names. This week’s bounce off that support pulled the price back into the upper half of its recent trading range, keeping the primary uptrend intact.

Volatility has cooled but not disappeared. After spiking into the upper 20s during the recent tech/AI downdraft, the VIX slid back into the high teens, around 16, by Friday’s close, signaling that the panic bid for protection is fading but that investors are not yet entirely complacent. That’s consistent with a market transitioning from a “shot across the bow” correction to a more typical year-end positioning grind.

Breadth is improving, but it isn’t a blow-out green light. Roughly 59% of S&P 500 stocks are back above their 50-day moving averages, and just over 61% trade above their 200-day, a solid improvement from the trough earlier in the month but still shy of the 70%+ readings you’d expect in a truly broad-based rally. Participation has also expanded beyond mega-cap tech, with more cyclical and value names stabilizing; however, leadership remains heavily tilted toward large-cap growth and AI-adjacent beneficiaries.

Bullish case heading into December:

Seasonality, positioning, and trend still lean in favor of the bulls. December is historically one of the stronger months for equities, particularly when the market is already up by double digits year-to-date. Expectations for a December Fed rate cut, and a gradual cooling of inflation, support the “soft-landing” narrative, while corporate buybacks and under-invested managers create fuel for a “chase into year-end” if resistance gives way. With volatility easing and breadth improving, the path of least resistance near term remains higher if key support zones are maintained.

Bearish case heading into December:

The bears will point out that valuations in AI and growth expectations remain stretched, that volatility is still elevated compared to the summer lows, and that breadth, while improved, is not confirming a runaway advance. The recent episode, where AI leaders and other risk assets (including Bitcoin) sold off together, is a reminder that risk appetites can shift quickly when the crowd questions the durability of earnings or the timing of Fed cuts. Delayed economic releases from the earlier government shutdown create an additional wildcard: a batch of weaker-than-expected data hitting all at once could challenge the soft-landing narrative just as liquidity gets thinner into year-end.

Support and Resistance Levels

Bottom line: the primary trend remains bullish, but the margin for error is narrowing. As we enter the final month of the year, the bulls remain in control as long as the index holds above the 50-day moving average and breadth continues to improve. A failure back below the 6,600 area, especially if accompanied by a renewed spike in volatility and renewed AI/credit jitters, would shift the balance of risk toward a deeper consolidation rather than a clean “Santa rally” into year-end.

Loading recommendations...