Every OEM in the world has two choices.

Choice One: Sell the Nvidia AI hardware and software stack and boost the top line while diluting operating income in their systems businesses.

Choice Two: Get basically no AI revenues at all excepting an AMD deal here and there and, in the case of Hewlett Packard Enterprise and Dell and Lenovo every once in a while, some fairly large system sales to HPC national labs every four years. Get nothing incremental above and beyond traditional server sales to enterprises, governments, and academia, riding the Intel Xeon and AMD Epyc upgrade generational waves.

Neither is a great option, but every OEM aside from IBM (which has its very own installed base and a unique and indigenous AI acceleration plan that does not involve either Nvidia or AMD) is smart enough to take Choice One because they need a story to tell and they also have hopes to sell incremental storage, networking, and services into the accounts where they get AI deals. Nvidia knows all of this, which is why it continues to accrue most of the margins in AI cluster sales, as its most recent financial results so clearly show.

Michael Dell is multi-billionaire in his own right, and attained that status because he is calm and smart, and importantly, also built the largest traditional datacenter equipment supplier in the world. And that is why Dell has managed to get the company that bears his name at the front of the line building the gear for some of the largest deals that are going down in AI, notably massive clusters at xAI and CoreWeave. It doesn’t hurt, either, that there is a desire to buy American to avoid the wrath of President Trump.

Let’s dive into the numbers and see what is happening in the datacenters that Dell serves.

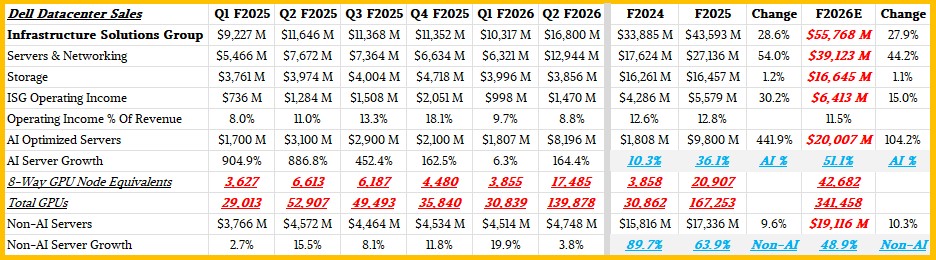

In the second quarter of fiscal 2026, which ended on August 1 (the quarter, not the year), Dell had $23.94 billion, up 26.3 percent year on year and up 36 percent sequentially, thanks in large part to some huge AI systems that were installed in the period. Services revenues, on the other hand, were down 3.8 year on year but up 1.1 percent sequentially.

All told, revenues were $29.78 billion, up 19 percent, with operating income of $1.73 billion, up 29.1 percent, and net income of $1.16 billion, up 38.4 percent. Still, despite all of that increasing enrisening as we drill down through the financials from top to bottom line, net income share of revenues was only 3.9 percent, with an “easy” compare with the year ago quarter when net income as a share of revenue was a paltry 3.4 percent.

Don’t blame the PC business. Dell’s Client Solutions Group had $12.5 billion in sales in Q2 F2026, up seven-tenths of a point, but net income was up 4.7 percent to $803 million, representing 6.4 percent of revenues and marking the highest level seen in the past seven quarters.

Thanks to the GenAI boom, Dell’s Infrastructure Solutions Group, which sells servers, storage, switching, and services into the datacenter, is finally – and very likely permanently – larger than its PC business for the first time in its history. (We are not counting the time a decade and a half ago when Dell ate Perot Systems and was also eating software companies to try to create a clone of IBM, much as HPE did at the same time.)

Dell sold $12.94 billion in servers and networking in fiscal Q2, up a whopping 68.7 percent and more than double sequentially. Storage sales were down 3 percent to $3.86 billion, and Jeff Clarke, Dell’s chief operating officer, said on a call with Wall Street analysts going over the numbers that hyperconverged infrastructure customers were doing “a rethink of their private cloud options” and added that Dell had recently announced an offering to help customers use an “open, disaggregated, automated alternative.”

Add it up, and ISG had $16.8 billion in sales, up 44.3 percent year on year. But operating income only rose by 14.5 percent to $1.47 billion, representing 8.8 percent of revenues. This is the lowest level in the past five quarters. (Don’t get us started talking about eating bear meat and starving to death. . . . ) ISG’s average level of operating margin in the prior two years was 12.5 percent, which strongly suggests that ISG is not making a lot of money on its current AI system deals.

Dell had pretty good AI server sales in the year ago period, at $3.1 billion, but this time around in Q2 F2026 AI system sales were up by a factor of 2.6X due to some deals with neocloud CoreWeave as well as other enterprise customers, hitting $8.1 billion in the quarter. Dell’s AI system backlog was $11.7 billion as it exited the quarter, down from $14.4 billion in the prior quarter but 3.1X higher than when the year ago quarter closed.

“We had the best quarter we have had in AI with enterprise customers in Q2,” Clarke said on the call. “The number of customers grew, the largest dollar demand that we had to date in enterprise. And I think that bodes well for the future, and particularly in enterprise, where we have the opportunity to sell networking, storage, and services with AI factories.”

If you do the math, Dell’s tradition PowerEdge server (and networking) business rose by 3.8 percent in Q2 F2026, to $4.75 billion. Dell’s AI server business was much larger than its traditional server business in this quarter, but it may not stay that way given the lumpiness of AI cluster sales and the fact that the X86 server business is overdue for an upgrade cycle.

Elaborating further, Clarke said this:

“As we look at the pipeline, again, I think it’s important for us to make sure we communicate clearly our sovereign part of the pipeline and our enterprise part of the pipeline grew double digits and grew faster than the CSP portion of the pipeline. That pipeline now has over 6,700 unique customers as opportunity for us. And the composition of that is predominantly Blackwell. Encouraging, we’re seeing the new RTX 6000 in that portfolio, and we’re seeing air-cooled and PCI-Express as a result of that in the pipeline, which are very good indicators of enterprise opportunity.”

“It is a composition of CSP from a customer point of view plus enterprise plus sovereign. It’s predominantly from a technology point of view. Blackwell with a growing demand of PCI-Express options. And then if I go back to your question about margins, we expect the one-time cost in our supply chain to reconfigure into expedited materials not to be in place in the second half.”

“We think there’s some opportunity for us to continue to value engineer the scaling of the P and L. And then, lastly, the enterprise customers and shipping to enterprise customers and the opportunity to attach unstructured storage, networking, and our professional services around that.”

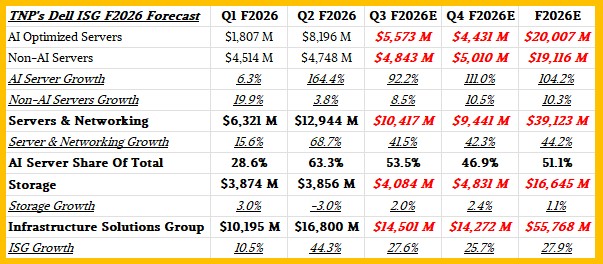

That brings us to the forecast for fiscal 2026, which was updated by Dell and which forced us to tweak our model.

Dell now says it will have at least $20 billion in AI system sales in fiscal 2026, and we think the year might look like this now:

So fiscal Q2 is going to be a peak for the company’s AI server business, but it looks to us like with a reasonably healthy uptick in traditional servers – over 70 percent of the systems in the Dell base are two generations back or older – these two halves of the Dell server business will be more or less at parity for the year when it all averages out. (We are giving AI servers slightly more sales, but that is subject to change if the enterprise server upgrade cycle turns out to be a little stronger.) Dell has only said that ISG will grow at the middle to high 20 percents for the year as guidance.

Here is a wider view of Dell’s system business with the forecast in it:

Just for fun, we calculate eight-way GPU node equivalents and then how many GPUs that would represent. These figures are not meant to be precise, but illustrative so you can get your head wrapped around the order of magnitude of the shipments Dell is doing for AI servers.

If this was all done with GB200 NVL72 or GB300 NVL72 rackscale systems, the number of GPUs estimated would represent around 2,325 racks in Q1 F2026 and around 4,750 racks in Q2 F2026. This may sound like a lot until you realize Nvidia is making enough Blackwell system chippery and assembling it through partners to drive 1,000 racks per week just for the GB300 systems alone.