Housing affordability is at its worst in decades, but a new Goldman report suggests some of the most severe pressures may begin to ease, offering modest relief in the years ahead. That's welcome news for prospective homebuyers who've been priced out by soaring home values and the Federal Reserve's aggressive interest rate hiking cycle.

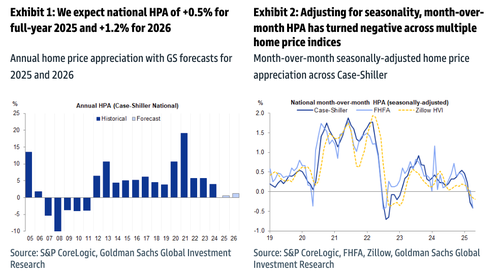

"We are lowering our forecasts for U.S. home price appreciation over the next two years," analyst Vinay Viswanathan wrote in a note to clients. He cut the firm's national home price appreciation (HPA) forecast from 3.2% to .5% in 2025, and from 1.9% to 1.2% in 2026.

Viswanathan outlined three specific drivers that underpinned his decision to revise the HPA forecast down:

First and foremost, recent home price index data has deteriorated, likely reflecting a drop in demand. Case-Shiller, FHFA, and Zillow indices all gauged negative sequential HPA in March, April, and, based on Zillow's higher frequency estimates, May (Exhibit 2). Though some of the weakness can likely be attributed to the acute tariff concerns earlier in the year (which equity prices and, to a lesser extent, consumer sentiment suggest are subsiding), the decline in May consumer spending is evidence that an uncertain growth environment is influencing household financial behavior.

Second, the lack of supply that previously bolstered strong HPA is gradually recovering. While most metrics suggest that aggregate supply is still far from overwhelming demand, for-sale inventory of existing homes is approaching pre-COVID levels while for-sale inventory of newly constructed homes is at levels last seen in 2009.

Third, we see only limited scope for mortgage rates to decline in a softer growth environment, and our base case is for mortgage rates to decline by only 20-25 bp through the end of 2026. We do not see the pullback in immigration as a major risk for single-family HPA given the likely low headship rate for the humanitarian/undocumented immigrants most affected, but there could be a larger impact on multifamily rents.

The analyst emphasized that this does not signal a significant downturn in prices, writing: "...but meaningful national home price declines remain unlikely."

What caught our attention in the 33-page report was the section outlining modest affordability relief for prospective homebuyers. This is especially important for the folks who've been sidelined in recent years because of higher prices and elevated rates.

"Mortgage rates will likely grind lower," Viswanathan wrote in the report, with the 30-year conforming mortgage rate forecasted to end the year at 6.5%.

Viswanathan continued, "Alongside a downtick in mortgage rates, the growing gap between income growth and HPA should help slightly improve housing affordability, albeit remaining historically poor..."

How many young people are still on the sidelines? A lot....

According to Census Bureau data, about a third of all 18- to 34-year-olds are still living in their parents' basements or attics.

And this.

Real estate agents and mortgage originators are praying for a new Fed chief who'll slash rates and bring life back into an industry crushed by Fed Chair Powell.

More here from Goldman's Research team available to pro subs.

Loading...