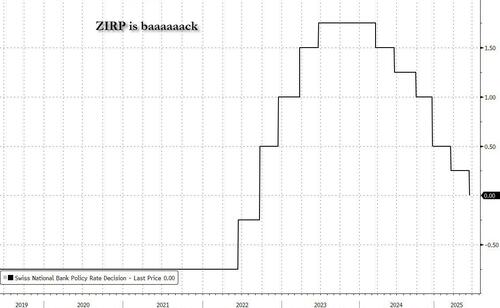

Five years after covid sparked a once in a generation inflationary surge and forced all central banks to push their interest rates well above the zero (and in some cases negative) lower bound which defined the post-QE era, overnight the Swiss National Bank became the first to show that the world of higher rates is over and ZIRP is coming back, after the central bank cut its rate from 0.25% back to 0.00% for the first time since 2022.

But it's not just ZIRP that is back: NIRP is also here courtesy of the Swiss, because while the SNB may have cut its interest rate to zero, the way it penalizes banks’ excess reserve holdings means lenders will face negative rates if they park too much cash at the central bank.

Ah yes, the magic of the zero lower bound is once again with us!

According to a statement by the SNB published on Thursday morning, Swiss banks can hold up to an unchanged 18 times their minimum reserve requirement in sight deposits at the SNB for free but anything over that they will be charged interest of -0.25% as the discount from the policy rate remains unchanged at 25 basis points.

The goal behind the “tiered remuneration”, according to Bloomberg, is to incentivize lending between banks so that enough liquidity is exchanged on the Swiss money market. For lenders holding more than their limit it’s cheaper to pass on excess reserves to institutions which are under their thresholds, because they have to pay them less than the central bank.

For all lenders which don’t have a minimum reserve requirement the threshold is set at a paltry 10 million francs ($12 million) in sight deposits, the SNB said.

The system, which the SNB has had in place since it lifted its key rate above zero in 2022, means that the average money-market rate — known as Saron — has usually been a few basis points below the central-bank rate.

Which means that starting Friday, negative funding costs for banks are therefore likely, as board member Petra Tschudin told reporters in Zurich. She added that she expects only “very little” sight deposits to be remunerated at the negative rate. That chimes with experience from some three years under the regime, where typically only a tiny fraction of them were hit by the lower rate.

Still, little or not so little, negative rates are back in at least one country... and soon in many more.

While Switzerland’s main banks lobby called the SNB’s decision “understandable,” it criticized its consequences.

“It’s clear that a zero interest rate environment diminishes the incentive for responsible saving and places additional pressure on retirement provision,” the Swiss Bankers Association said in a statement. “As in previous periods of low interest rates, banks and their customers once again bear a significant share of the monetary policy burden.”

Similarly, the insurance association welcomed the SNB not going negative, but stressed that “even the return to a low interest rate environment already poses a challenge” to the sector.

SNB President Martin Schlegel acknowledged the discomfort the new rate environment creates for banks and signaled that there’s an elevated bar for further cuts.

“We would not take the decision to go negative lightly,” he said. “But I want to stress that the profitability of banks is not within the national bank’s objectives.”

Finally, while some argue that negative rates are a way for capital deficient central banks to restock their coffers after years of high rates pushed them all into technical insolvency, given the small share of deposits affected, it’s unlikely that the SNB will make a lot of money from charging lenders. Between 2015 and 2022, the central bank earned almost 12 billion francs from negative rates, though it then paid out 14.5 billion francs from when rates turned positive through the end of March of this year.

Loading...