Ford shares jumped before tumbling after hours on Monday, as the legacy automaker reported guidance that was on the low end of expectations. Like many other automakers, Ford continues to grapple with balancing the costs of EV production, high interest rates and a tapped out American consumer.

Ford announced third-quarter revenue of $46 billion, with net income totaling $0.9 billion. This figure includes a $1 billion charge related to its electric vehicle business, which the company had previously disclosed. Adjusted earnings before interest and taxes (EBIT) for the quarter came in at $2.6 billion.

Here are all the company's Q3 figures versus estimates, via Bloomberg:

-

Total Revenue: $46.2 billion, up 5.5% year-over-year (y/y), surpassing the $43.07 billion estimate.

- Ford Blue Revenue: $26.2 billion, exceeding the $24.63 billion forecast.

-

Ford Model e Revenue: $1.2 billion, below the $1.42 billion estimate.

-

Ford Pro Revenue: $15.7 billion, above the $15.28 billion projection.

-

Adjusted EPS: 49 cents, matching analyst expectations.

-

Adjusted EBIT: $2.6 billion, up 18% y/y, though below the $2.77 billion estimate.

-

Adjusted EBIT Margin: 5.5%, improving from 5% y/y but short of the 6.3% forecast.

-

Ford Blue EBIT: $1.63 billion, missing the $1.77 billion estimate.

-

Ford Model e EBIT Loss: $1.22 billion, smaller than the expected loss of $1.34 billion.

-

Ford Pro EBIT: $1.81 billion, outperforming estimates.

The automaker's Ford Pro division saw solid growth, with revenue rising 13%. Additionally, Ford Pro Intelligence, the company’s paid software service, reported a 30% increase in subscriptions, reaching nearly 630,000 users.

Ford also declared a regular fourth-quarter dividend of 15 cents per share. For the full year of 2024, the company now expects adjusted EBIT to reach approximately $10 billion.

Ford revised its full-year 2024 outlook, now projecting adjusted earnings before interest and taxes (EBIT) of approximately $10 billion. This is a narrowing from its previous guidance of $10 billion to $12 billion. However, the automaker maintained its forecast for adjusted free cash flow, which is expected to remain between $7.5 billion and $8.5 billion.

Here's a full look at its year forecast:

- Adjusted EBIT: Now expected to be $10 billion, down from the prior range of $10 billion to $12 billion, and below the Bloomberg consensus estimate of $10.63 billion.

- Ford Pro EBIT: Forecast unchanged at $9 billion, compared to the prior range of $9 billion to $10 billion.

- Ford Blue EBIT: Now expected at $5 billion, down from the previous range of $6 billion to $6.5 billion.

- Ford Model e EBIT Loss: Projected to be $5 billion, in line with earlier guidance of a $5 billion to $5.5 billion loss.

- Ford Credit EBT: Anticipated to reach approximately $1.6 billion.

- Capital Expenditure: Revised to $8 billion to $8.5 billion, compared to the previous forecast of $8 billion to $9 billion, and close to the Bloomberg consensus estimate of $8.39 billion.

- Adjusted Free Cash Flow: Maintained at $7.5 billion to $8.5 billion.

Ford President and CEO Jim Farley said: “We are in a strong position with Ford+ as our industry undergoes a sweeping transformation.”

He added: "We have made strategic decisions and taken the tough actions to create advantages for Ford versus the competition in key areas like Ford Pro, international operations, software and next-generation electric vehicles. Importantly, over time, we have significant financial upside as we bend the curve on cost and quality, a key focus of our team.”

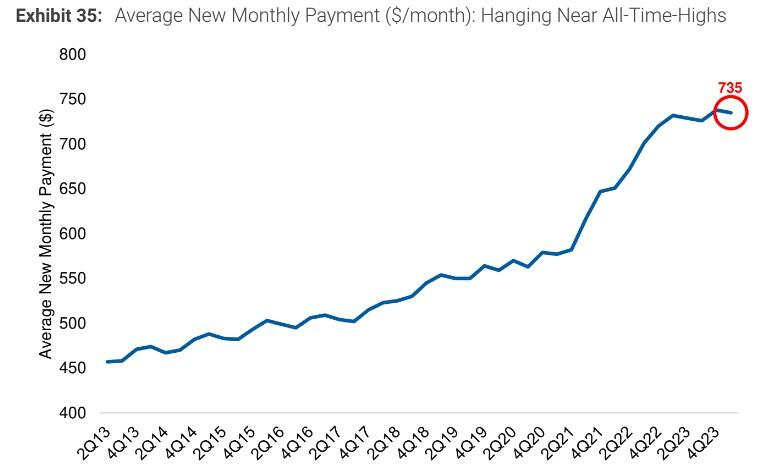

Recall last month Morgan Stanley's Adam Jonas had downgraded Ford on Chinese supply and rising delinquencies. Jonas mentioned affordability concerns in the U.S. market, claiming it is highly stretched, with inventory levels now back to pre-COVID norms.

Meanwhile, Auto Asset-Backed Securities (ABS) data shows a growing proportion of consumers are staying delinquent for longer, with higher severity rates. Although subprime defaults are lower in 2023 compared to 2022, prime defaults have increased.

The capital intensity required to compete in Advanced Driver Assistance Systems (ADAS) and Autonomous Vehicles (AV) is often overlooked, Jonas says. As the AI and data themes gain traction in the automotive sector, automakers will need to invest tens of billions in proprietary AI models.

Ford Vice Chair and CFO John Lawler commented: “We are remaking the company with Ford+ into a higher-growth, higher-margin, more capital-efficient and more durable business.”

“The work we have done over the past few years to restructure our global business -- and tailor our product lineup to segments where we know our customers best -- is driving continued growth and generating stronger and more consistent cash flow," he added.