By Peter Tchir of Academy Securities

In the Old Days…

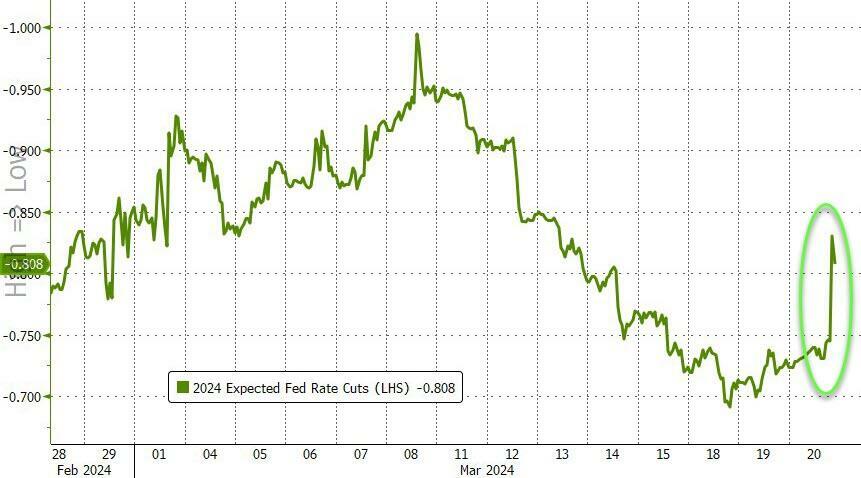

The bond market (and stocks) both interpreted the “unchanged” in median for dots for 2024 as a sign the Fed was committed to 3 cuts.

Two things immediately popped out to me:

- The average went from 4.7% to 4.81% as the distribution changed dramatically. Only 1 person thought there should be 4 cuts, as opposed to December when 5 thought more than 3 cuts, including one member who had 6 cuts.

- In 2025 the median priced out one less cut and the average moved 17 bps higher. Not in the end of the world, but closer to higher for longer, than a quick easing cycle.

Under normal circumstances, would have said to fade initial reaction, but nowadays, it all comes down to the presser, which is where all the “fun” is.

Balance Sheet Reduction

The Fed admitted they are getting closer to slowing the pace of quantitative tightening (QT). This makes sense, as I’m told there is a limit to how small their balance sheet can get (due to bank reserves, I believe). So it shouldn’t be a surprise and sounds like something we might get more information at next meeting. It would, in my opinion, be easier “politically” to shrink QT into the election, rather than cutting rates.

Should be a positive for risk assets and yields, though balance sheet run-off seems to have been less impactful than large scale asset purchases, where they bought duration, having a far bigger impact than just letting debt mature and not buying more.

Lags and Belief in Inflation Being Under Control

The cutting argument, now seems to largely be based on the belief/hope that inflation is coming down and will continue to come down, despite some recent higher than expected prints. They are definitely worried that if they don’t cut now, they might be behind the curve. The case to cut seems more about lag time and risks of moving too late, rather than strong conviction things are under control (different tone than the December meeting).

What Now

As the press conference finishes, we’ve moved up timing of cuts (June almost certain) and back to more than 3 cuts this year. The former makes sense, the latter less so.

The 30-year bond has a slightly higher yield on the day (that seemed to move in the “right” direction) given all the noise and comments.

Dollar down (not hawkish Fed), bitcoin and stocks higher! Stocks seem to like discussion about QT and rate cuts (though since they are “long duration assets”, not sure why they quite as responsive as they are).

Another day of watching some market leaders trade somewhere in between meme stocks and ARKK, circa 2021.

Maybe this was the “all-clear” we need to take Nasdaq 100 to new highs? Except, we are kind of left more data dependent than it felt back in December.

I expect bond yields, which “survived” the potentially very dovish Fed, to resume their march higher (led by 10s and longer).

Maybe I’m being stubborn, but stocks seem to be behaving like “stonks” again, but not sure what pushes them out of what has become a range, while I can still see many things leading to a sharp, rapid pullback.