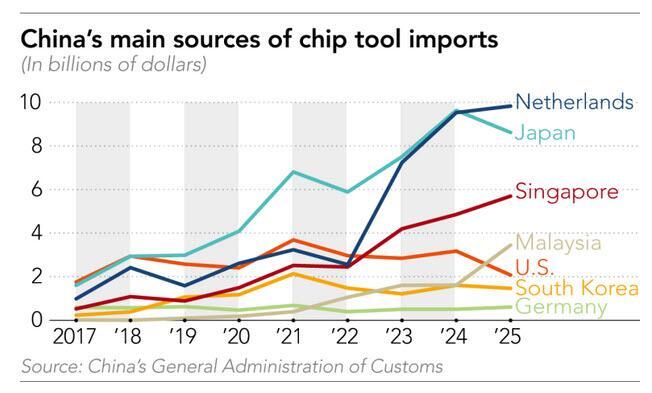

China's imports of chipmaking equipment from Malaysia and Singapore rose sharply in 2025 to surpass those from the US, which sank to an eight-year low, an analysis by Nikkei Asia has found - even as American companies remain a vital source of advanced tools for the country.

While the Netherlands and Japan remain China's primary foreign sources of critical semiconductor manufacturing machines by shipment origin, imports from the two Southeast Asian countries reached record levels: $5.7 billion for Singapore, up more than 17% year over year, and $3.4 billion for Malaysia, more than double the 2024 figure.

Direct imports from the US, meanwhile, declined more than 34% to about $2 billion, the lowest level since 2017, according to Chinese customs data. The decline was to be expected following President Trump's return to the White House, as he sharply limited access of US semiconductors to China, although tensions began earlier. Since Trump's first term and during the subsequent Biden administration, the US has raised tariffs and imposed fresh export controls aimed at slowing China's advances in chipmaking technologies for defense, space and artificial intelligence applications.

Despite the decline, the Chinese market remained a critical revenue source for leading US chip equipment makers last year. Applied Materials, Lam Research and KLA all earned more than 30% of their total sales from China in fiscal 2025.

Charles Shi, a veteran semiconductor analyst with Needham & Co., told Nikkei Asia that the uptick in China's imports from Southeast Asia is mainly due to the large number of U.S. chip equipment makers expanding manufacturing capacity in the region to better serve non-U.S. clients.

"Lam Research is building significant manufacturing capacity in Malaysia as they work to meet growing equipment demand beyond what their U.S. manufacturing capacity can serve," Shi said. "Singapore has been a popular destination for [the] U.S. equipment industry to go overseas. For example, both Applied Materials and KLA have been manufacturing in Singapore."

The three top U.S. chip tool makers generated nearly $19 billion in combined revenue from China in fiscal 2025, significantly exceeding figures implied by customs data based on where shipments originated from and underscoring the effectiveness of American vendors' production diversification strategies. Nikkei Asia first reported their production shift toward Southeast Asia in early 2023.

For ASML of the Netherlands, China's share of revenue came to 29.1% in 2025, while the figure for top Japanese chip tool maker Tokyo Electron was more than 40% for fiscal 2025.

Anticipating major chip wars, over the course of 2020 to 2025, China's accumulated chip tool imports from Japan reached more than $42 billion, followed by the Netherlands' $35 billion . Japan is home to many top chip equipment makers such as Tokyo Electron, Screen Semiconductor Solutions and Ebara, while the Netherlands has the world's largest chip equipment maker, ASML, as well as key suppliers such as ASM, an atomic-level deposition tool specialist, and Besi, a maker of advanced chip packaging tools.

Meanwhile, China's domestic chipmaking equipment makers are experiencing a once-in-a-generation surge in growth, driven by Beijing's push to foster homegrown tools and reduce reliance on foreign technologies. Top suppliers all reported record revenue and profits for 2025, led by Naura, Advanced Micro-Fabrication Equipment Inc. China (AMEC), ACM Research and Piotech.

Naura, China's answer to Applied Materials, has seen its revenue balloon from 6.05 billion yuan ($887 million) in 2020 to 27.14 billion yuan in the first three quarters of 2025. Revenue for AMEC skyrocketed more than 400% from 2020 to 2025. Piotech, a thin-film deposition chip tool specialist, has seen its revenue grow 13 times between 2020 and 2025.

Shi of Needham said China has made good progress in fostering local chip tool makers, but internal competition is intensifying. "While leading domestic equipment companies are still posting strong revenue growth, there are indications that their margin performance is deteriorating," Shi said of Chinese chipmaking companies. "We believe intensifying domestic competition might have forced domestic equipment companies to 'race to the bottom' by undercutting each other's prices."

With China's equipment suppliers becoming more competitive in recent years, US policymakers are seeking to further close loopholes in export rules. In April, bipartisan lawmakers introduced the MATCH Act, which calls on "multilateral allies" to coordinate more closely in aligning and tightening export restrictions across key segments of the chipmaking equipment industry. These measures would further target critical "chokepoint" components and machinery, as well as shipments to leading Chinese memory and logic chipmakers, including CXMT, YMTC, SMIC and Hua Hong.

"Chinese tool companies on the Entity List are unable to get access to U.S. parts, but there are many parts that Europe and Japan can backfill, and that's the conundrum that we find ourselves in today," Kevin Kurland, a former official at the U.S. Department of Commerce and current senior advisor at Beacon Global Strategies, told Nikkei Asia. "If controls don't get aligned multilaterally with allies, U.S. controls can undercut American companies' competitiveness while allowing Chinese companies to continue to function and operate - a lose-lose outcome.

Alex Rubin, a former CIA China analyst and visiting fellow at the Hoover Institution, told Nikkei Asia that "component export controls definitely make sense."

"It's very similar to what we are seeing in commercial aviation: China is assembling the finished C919 aircraft, but is sourcing parts from U.S. and European suppliers. Chinese companies are trying to compete with Boeing and Airbus, while sourcing from a similar supply chain," Rubin said.

While China is still massively sourcing foreign chip tools, its ultimate goal is self sufficiency, industry sources say.

While durability, reliability and performance may not be at the same level, "for every foreign chipmaking tool, material and component you can think of, you could find Chinese versions," said an executive with a Taiwanese chipmaking tool who participated in the Semicon China industry event in late March. "Chinese chipmakers will continue to buy foreign solutions while they can, but there's no doubt about the country's will to increase the use of homegrown suppliers."

"China is adopting a two-way approach: developing homegrown tools while continuing to purchase foreign equipment whenever possible. Since imported tools often offer better performance, they are still buying aggressively -- and even repurposing consumable parts from one piece of equipment to repair other chipmaking machines," another chip industry executive with knowledge of the matter told Nikkei Asia.

A third executive with a Chinese chipmaking tool supplier told Nikkei Asia that the aggressive expansion plans by Chinese logic and memory chipmakers have given local vendors more opportunities to break into and secure a position in the domestic supply chain.

Nikkei Asia was the first to report that Chinese top chipmakers led by SMIC, Hua Hong and Huawei-linked chipmakers are aiming to aggressively expand advanced chip production capacity, including on the performance level of 7-nanometer or even 5-nm technologies, to support the rise of domestic AI chip developers. Meanwhile, top Chinese memory chip producers CXMT and YMTC are launching their largest expansions in response to the unprecedented global memory crunch amid the AI boom, Nikkei revealed in early February.

American allies such as the Netherlands and Japan have already introduced rules to align with U.S. export controls, but policymakers in Washington feel those restrictions are still much too loose. The U.S. has imposed multiple rounds of regulation on exports to China and has added many leading Chinese chip equipment suppliers and chipmakers to its Entity List.

The MATCH Act, if passed, could further limit global vendors' ability to supply critical tech to China. The bill targets some older - though still critical - generations of chipmaking machines as well as components, both of which can be chokepoints for China's efforts to build up its domestic chip industry. Introduced in early April, the bill still needs to go through the legislative process, and it remains unclear how the Netherlands, Japan and other countries would respond to any diplomatic pressure to comply. For example, only ASML in the Netherlands and Canon and Nikon in Japan can produce commercially viable lithography machines -- an area where China continues to face significant challenges.