There was much anxiety ahead of Oracle's Q3 earnings release: yes, revenue growth would be solid but would it come at the expense of even more capex, which has sent the stock price tumbling more than 50% since its record high on Sept 10. In the end, it turned out the company had learned from recent mistakes and projected a goldilocks future: strong revenue and just right capex.

Here is what Oracle reports for Q3:

- Adjusted EPS $1.79 vs. $1.47 y/y, beating estimate $1.70

- Adjusted revenue $17.19 billion, +22% y/y, beating estimates of $16.89 billion (Revenue in constant fx +18%, in line with estimate +18.8%)

- Cloud revenue (IaaS plus SaaS) $8.9 billion, +44% y/y, beating estimate $8.84 billion (in constant currency +41%, estimate +41.7%)

- Cloud Infrastructure revenue (IaaS) $4.9 billion, +81% y/y, beating estimate $4.74 billion (in constant currency +81%, estimate +82.2%)

- Cloud Application revenue (SaaS) $4.0 billion, +11% y/y, in line with the estimate $4 billion (in constant currency +11%, estimate +11.6%)

- Software revenue $6.12 billion, +3.3% y/y, beating estimate $5.97 billion

- Software Support revenue $4.97 billion, +3.6% y/y, beating estimate $4.89 billion

- Software License revenue $1.15 billion, +1.9% y/y, beating estimate $1.1 billion

- Hardware revenue $714 million, +1.6% y/y, missing estimate $724.6 million

- Service revenue $1.44 billion, +12% y/y, beating estimate $1.36 billion

Of note here, sales in the company’s closely watched infrastructure business gained 81% to $4.9 billion in the period ended Feb. 28, the company said Tuesday in a statement. That marked a faster increase than estimate of 79% and compared with a 68% revenue rise in the previous quarter. Going down the line:

- Adjusted operating income $7.38 billion, +19% y/y, estimate $7.21 billion

- Adjusted operating margin 43% vs. 44% y/y, estimate 42.7%

- Remaining performance obligations $553 billion vs. $130 billion y/y

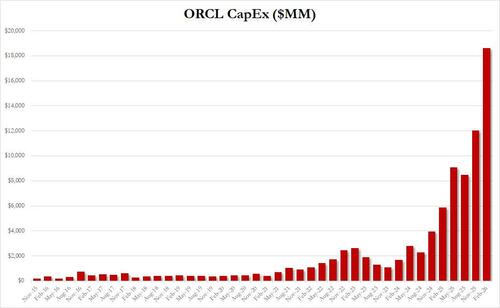

And while the above is all good, what wasn't so good is that ORCL's Q2 capex came in at a stunning $18.6 billion, triple the number from a year ago, and 50% higher than the Q1 capex print. To say that the company is incinerating money is doing a disservice to incinerators.

Elsewhere, the company's remaining performance obligation, a measure of bookings, were $553 billion, compared with the $523 billion reported in the prior quarter.

Looking ahead to the fourth quarter, the company's guidance range came above estimates:

- Revenues to grow from 18% to 20% in constant currency (grow 19% to 21% in USD):

- Adj. EPS to grow between 15% to 17% and be between $1.92 and $1.96, beating estimates of $1.95 (grow between 15% to 17% and be between $1.96 and $2.00 in USD)

- Cloud revenue to grow between 44% to 48% in constant currency (expected to grow from 46% to 50% in USD)

Adding across, this means that for fiscal 2026, Oracle expects revenue of $67 billion and capital expenditures of $50 billion, which is unchanged from our most recent previous guidance. Incidentally, there is no way in hell ORCL's full year 2026 CapEx is only $50 billion since its LTM capex is already $48.25 billion.

Perhaps most importantly, Oracle also published its fiscal 2027 guidance which is as follows:

- For fiscal year 2027, Oracle is raising total revenue guidance to $90 billion, beating estimates of $86.7 billion.

There was no mention of what 2027 capex will be, so expect some very pointed questions on the call because alongside massive capex comes just as massive cash burn, which, as shown below... is terrifying. As readers are well aware, the question for the past 6 months has been: just how much debt will ORCL need to fund it?

Cash burn aside, Oracle's earnings were solid, with the company posting cloud revenue that was better than expected and projected strong sales in the upcoming fiscal year, a sign the company is turning its massive AI bookings into revenue.

Oracle is working to deliver on massive cloud infrastructure contracts with customers like OpenAI and Meta. Known for its namesake database software, the company’s cloud business has found major success by providing chip-filled data centers and other equipment for training and deploying AI models.

The shares increased about 7% in extended trading after closing at $149.40 as the kneejerk reaction to the company's earnings was viewed as favorable. Let's see if this continues into tomorrow's session.

As a reminder, the stock has lost more than 50% of its value from a September peak as Wall Street has grown worried about the costs and logistics associated with the massive build-out.

Loading recommendations...